Now that mandatory climate-related financial reporting is the law of the land[1], liable entities – particularly Group 1 reporters – need to get cracking on their path to compliance.

Over the last 6 months, Energetics has been helping clients across a wide range of sectors prepare to build robust and defensible disclosures across the ~100-clause requirements of the draft Australian Sustainability Reporting Standards (ASRS). Meanwhile we have been tracking the passage of the legislation, the finalisation of the ASRS and the development of an assurance approach.

Our insights from this work builds on those we gained from the 240+ companies that completed our Readiness Assessment[2]. Here’s what we’ve learned:

NO EXCUSES: The draft documents provided enough clarity for action

Companies that started their work based on the draft requirements will find few substantive changes in the final versions. (Notable difference are that there are now two mandatory temperature scenarios in the legislation; the draft accounting standards are being renamed AASB S1 (the voluntary sustainability one) and AASB S2 (the mandatory climate reporting one),and have been revised to more closely align with their international counterparts, IFRS S2 Climate-related Disclosures; consultation on a draft assurance regime is imminent).

But the first stages of prep don’t depend on the finer points of the documentation. Getting all the relevant functions within the business to understand what the new reporting regime is and what it’s for, defining your approach to the first few disclosures and confirming an action plan, allocating resources and responsibilities – this all takes time and needs to be set in train as soon as possible.

Companies that have taken these steps are now well-placed to deal with the finalised details. If you were waiting for the legislation you have lost valuable months, so you need to use it coming into law as a catalyst to move fast.

LOTS TO DO: Even the minimum viable product requires a lot of hard work

Even entities experienced in reporting against the TCFD recommendations haven’t dealt before with many of the requirements in the AASB S2, particularly the challenging aspects of the Strategy section.

In addition, while technical compliance can in some cases be achieved by disclosing gaps – for instance, theoretically you could comply with the governance criteria by noting that your entity doesn’t have any oversight of climate-related risks, or you could choose not to develop responses for any financially material climate risks your entity faces – in practice most companies don’t want to do this, particularly if their peers have clearer disclosures in these areas.

This means that even your MVP will have to address all the AASB S2 sections, even if you do choose not to implement a few of the more discretionary elements (such as internal carbon pricing, remuneration for climate-related performance).

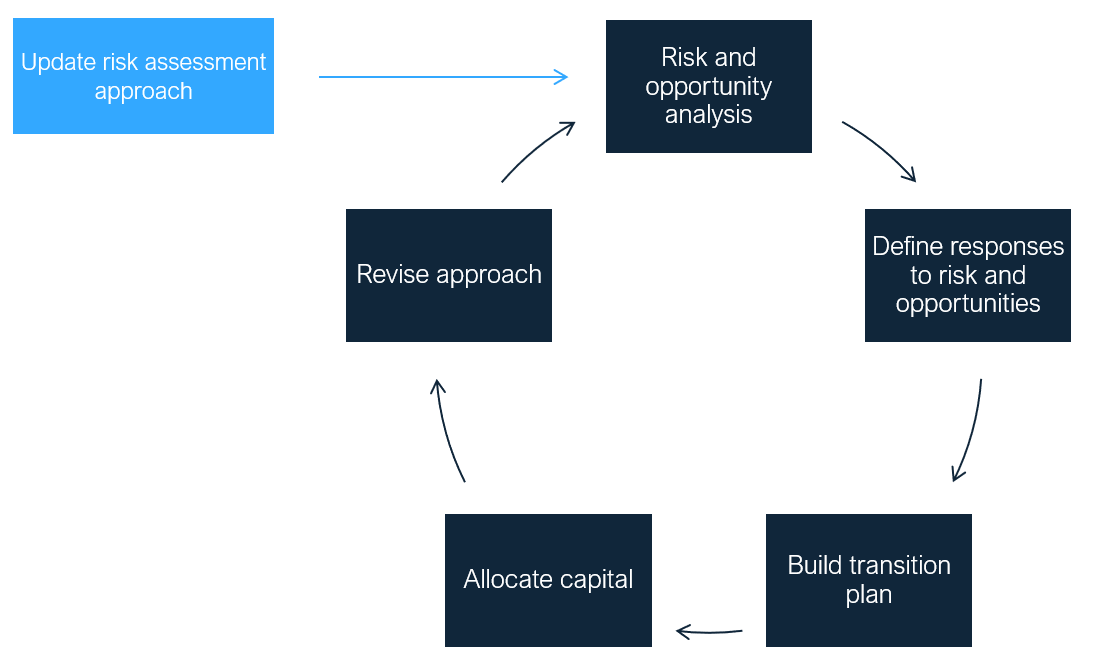

DO YOUR RISK ANALYSIS PROPERLY: The core of your disclosure depends on an iterative process of progressively more sophisticated risk and opportunity analysis

Your response to AASB S2 requires a thorough understanding of climate-related risks and opportunities, not just to your operations but upstream and downstream as well. You need to understand where your risks are concentrated across your business model and value chain, over three strategic timeframes. You need to define metrics to track these risks and your performance against them. You don’t need – but you will want – to define actions to reduce your risks and capture value from the opportunities. You don’t need to – but you may as well – roll these actions into a coherent strategy and call it a transition plan. And then you need to make a claim about your entity’s resilience to these risks.

Your process will look a bit like this:

Risk analysis should be sharpened within the annual process and over subsequent years.

While the legislation mandates a 1.5oC scenario and a >2.5oC scenario, you should seriously consider doing more than these – many significant risks are most likely to emerge somewhere between the bookends. Disorderly transition risks, and impacts resulting from the interaction of physical and transition risks, live in this space.

FINANCIAL MATERIALITY IS EVERYTHING: Financial materiality galvanises cross-functional support and should drive resources accordingly

ASRS requires only financially material information. This is not quite the same as “disclosure only of financially material risks”. The question of where financial materiality ends requires agreement across sustainability and finance risk, legal and strategy functions. Bridging the divide between the sustainability paradigm and the finance paradigm isn’t easy but will strengthen both.

Anything that’s not financially material (too fluffy or too small to matter) can be excluded from the disclosure process. But if climate risks and opportunities are financially material you will need to have very robust approaches in place not just to understand and disclose them but to address them.

When you understand and act on climate risk you build company value

Climate risks and opportunities are found in every industry and will impact every business, directly or indirectly. If you can leverage mandatory climate reporting to drive risk mitigation and value creation, you’ll get a lot more out of the exercise than compliance alone.

ERM and Energetics have undertaken ASRS gap analyses for Group 1 reporting clients in all sectors of the economy. We have worked with over 50+ companies to integrate climate risk management into their businesses and disclosures. We go beyond providing independent advice. What sets us apart is our deep technical expertise that is delivered throughout our end-to-end ASRS service. Our approach leverages clients’ existing work, together with tailored tools to help companies meet ASRS requirements – efficiently and effectively. The solutions we develop are actionable, from capacity building to executive strategy to operational execution.

[1] technically, the Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Bill 2024 has passed the House of Representatives, but only becomes an Act once it receives Royal Assent.

[2] You can take one of Climate-related Financial Disclosure Readiness Assessments (ASRS and ISSB) here.

Related insights

-

Mandatory climate disclosures Australia’s new mandatory climate-related reporting regime – how is it shaping u…READ MORE -

Physical risk analysis Climate disclosures should be assessed against the first National Climate Risk A…READ MORE -

Mandatory climate disclosures Australian business is ready to report on climateREAD MORE

Get our thought leadership directly to your inbox

Keep up to date with the latest insights on net zero, climate resilience and clean energy transition.