Just over 5 years remain for New South Wales to achieve its target of halving greenhouse emissions, and for the Federal Government to deliver on its commitment of 82% renewable electricity.

The challenge of reaching these 2030 targets is daunting, especially when we consider:

- Nearly 4 years have passed since the NSW Government legislated the Electricity Infrastructure Investment Act (EII Act) to enable the Electricity Infrastructure Roadmap[1]

- It’s been 2 years since the Albanese Government’s landmark climate change legislation set the 2030 target[2].

In this time much of the focus has been on laying the regulatory foundations for the clean energy transition. At the start of 2023 we saw some momentum created with Long Term Energy Service Agreement (LTESA) and more recently Capacity Investment Scheme (CIS) auctions, although noting most of the beneficiaries of these auctions have not been new projects brought forward. Most were committed at the time of the award.

Delivering the energy system of the future will depend on doubling transmission lines over the next 20 years[3].

Much of this is needed to connect new Renewable Energy Zones (REZs)[4] which will host the lion’s share of new variable renewable energy (VRE) capacity.

In this article ERM Energetics discusses the challenges facing the build out of renewables, and the benefits of accelerating and expanding the transmission capacity of REZs to keep renewable energy investment capital committed in Australia. We also consider the areas of opportunity for renewable energy investors.

Global and domestic headwinds are slowing the energy transition

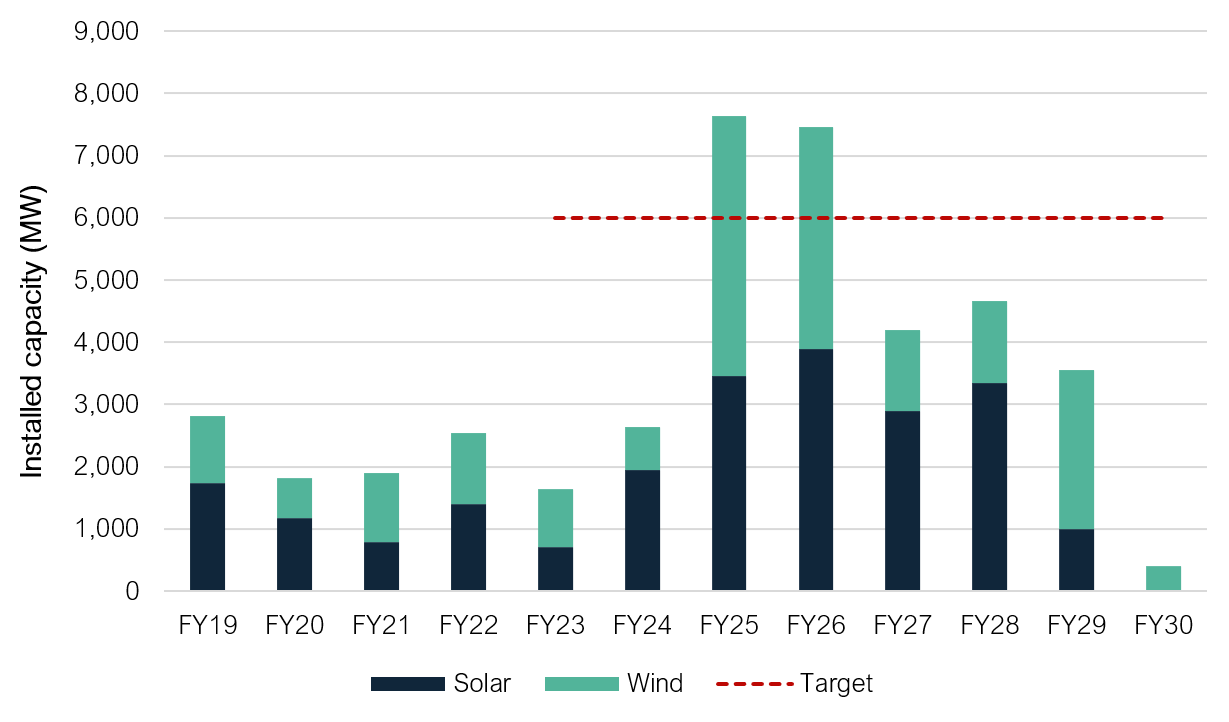

To achieve the Federal Government’s renewable electricity target, an average of 6GW[5] per annum of new VRE capacity[6] must be added between FY23 and FY30 to the 16.4GW[7] wind and solar capacity currently installed in the National Electricity Market (NEM). This is more than double the annual average of ~2.5GW of new utility-scale renewable capacity delivered between FY22 and FY24.

However, in recent years, the timelines for the development, construction, and commissioning of new renewable generation assets, especially wind, have blown out. This trend is not expected to change anytime soon. Industry faces significant challenges such as the rising cost of capital, global competition for equipment, global supply chain constraints, network connection and commissioning delays, domestic skills shortages and a lack of community support delaying planning approvals. These problems are impacting both the development of renewable energy generation and storage projects, and transmission networks.

Based on ERM Energetics’ assessment of new VRE projects delivered in the NEM since the start of FY23, Australia is delivering new capacity at half the pace required to meet the national 2030 target.

Furthermore, based on current estimates, new VRE capacity will only exceed the required NEM annual build out target in FY25 and FY26, falling short in all other years (see Figure 1 below) [8].

Figure 1: Development pipeline of on-shore wind and solar projects in the NEM - Anticipated* from FY24-30 based on (ERM Energetics dataset)* Anticipated includes in commissioning, committed and advanced projects

Figure 1 also assumes that additional VRE hosting capacity is delivered as planned to support the development pipeline.

While progress is being made with, for example, the successful tendering of the Central-West Orana (CWO) REZ transmission link by EnergyCo in NSW, there is a 4+year delay in delivering Snowy 2.0[9] and 2+year deferment of the operation date for the CWO REZ[10] transmission infrastructure project. Furthermore, limited progress has been made to unlock the critical Northern NSW REZs (Hunter-Central Coast and New England in latest ISP) with the route selection for the New England REZ Transmission Project only scheduled for 2025.

![]()

Figure 2: Key NSW transmission infrastructure projects[11]

Policy support is at an all-time high, but progress remains slow

Fortunately, we are seeing an unprecedented alignment between Federal, State and Territory Governments which are all supporting the energy transition away from thermal generation sources, and coal in particular. The collaboration by governments to implement the expanded Capacity Investment Scheme (CIS) announced in November 2023 is a case in point.

The successful implementation of the expanded CIS is crucial, as the targeted 32GW investment capacity – 9GW dispatchable and 23GW VRE – is needed to achieve the NSW and Federal Government 2030 renewable energy targets. During the latest auction for 6GW generation capacity[12], 2.2GW was reserved for NSW[13]; the outcome is expected to be announced in December. Whilst encouraging, not all the global and domestic factors causing the delays can be directly influenced by CIS auctions, it is increasingly evident that new capacity will lag for some years (see Figure 1).

As a result, the NSW Government has supported the extension of the 2.88GW Eraring Coal Power Station’s operation from 2025 to at least 2027 for at least two units, with permanent closure slated for 2029. Even though there is potential for electricity prices to fall in the near term (due to the additional supply retained), this decision comes at a significant cost to taxpayers and the environment. Further, lowering medium term market prices will only add to the difficulties faced by renewable energy investors, already struggling to reach financial close in a high-cost investment environment.

In short, this price effect works against accelerating the clean energy transition.

What can investors do to unlock the potential of NSW’s renewable energy assets?

Potential NSW VRE projects in various stages of development far exceed the hosting capacity[14] of the existing and proposed network. Mitigating the investment risk in this highly competitive market is dependent on increasing that hosting capacity.

But waiting for governments to deliver new REZ transmission infrastructure only risks VRE projects being delayed further.

In response to this challenging investment environment, innovative transmission models are emerging.

The concept of a Virtual Transmission Line (VTL) has been introduced by the Victorian Big Battery (VBB) in Geelong. The VBB has 250MW of its 300MW capacity reserved for a grid service contract, specifically over summer (nominally November to March). During this time, the VBB acts as a VTL by soaking up excess Victoria generation when the Victoria-NSW Interconnector (VNI) is unable to export energy to NSW (for reasons including interconnector capacity reached, system strength or stability issues).[15]

In NSW, this concept can help expand the Northern NSW transmission hosting capacity and support new investment in the area currently served by Eraring and Vales Point. These aging coal generators have a combined capacity of around 4GW, supplying the critical Sydney, Newcastle and Wollongong load centre areas. These generating assets are currently scheduled to retire between 2025 and 2029.

The Waratah Super Battery (WSB), like the VBB, operates under a System Integrity Protection Scheme contract to serve as a VTL. It expands the latent capacity of the existing transmission system connecting Sydney to the Hunter Valley and has an indirect impact on the CWO REZ capacity.

The WSB has 700MW of its 850MW capacity reserved for the grid service contract, which allows electricity consumers in the Sydney, Newcastle, Wollongong demand centres to access more energy from existing generators.

Virtual Transmission Lines – a new opportunity

For investors it is worth noting that the Capacity Investment Scheme, the CWO REZ and other access regimes, credit storage capacity bidders in merit assessments to the extent it is expected to reduce congestion/curtailment. This approach enables an increase in the hosting capacity of existing transmission infrastructure, meaning other VRE projects can dispatch more MWhs without the need for additional transmission capacity.

The role of VTLs can be expanded beyond REZs to support development of new infrastructure connecting to existing transmission lines.

Investors should assess opportunities for investment through a more holistic systems lens, rather than only looking at storage investment opportunities through a revenue stack lens. Beyond spot arbitrage and FCAS[16] revenue, we advise that investors explore the value of providing VTLs and the impact this could have on improved return on investment and competitive advantage.

ERM Energetics can help

Energetics, recently acquired by ERM, offers innovative, whole-of-market advice. Our approach integrates our experience across the electricity supply value chain and our deep understanding of policy developments and emerging technologies. We provide unrivalled market intelligence to support market entry, product development and portfolio strategy development. Our experts provide asset owners with:

- in-depth market insights and market-based valuations of projects / portfolios to support investment decisions or revenue strategy development, including applications for government support agreements (e.g. Capacity Investment Scheme and NSW Long-Term Energy Service Agreements in the NEM)

- the advice and analysis required to develop competitive products and offtake strategies

- sophisticated physical and financial hedging strategies to manage risk

- portfolio optimisation modelling, including valuation and commercial support for storage.

Please contact us for further information. For more information on ERM’s services to developers and investors click here.

[1] 12GW new renewable electricity generation by 2030 and 2GW long duration storage

[2] A key enabler of the Federal Government’s legislated 43% below 2005 by 2030 emissions reduction target.

[3] The AEMO ISP 2024 Step Change scenario anticipates the need for 10,000km of additional transmission in the NEM, stretching from Tasmania to Queensland. Grid capacity is forecast to expand from 57GW to 143GW (70 to 196GW with rooftop solar included) in 2040.

[4] Details of the zones identified by the three largest states can be found here: NSW, Victoria and Queensland

[5] AEMO| Draft 2024 Integrated System Plan

[6] Not including rooftop solar

[7] As at the end of FY23

[8] Our dataset represents more than 45% above and beyond the capacity projected in the AEMO generation information report as publicly announced, with estimated COD taking account of prevailing hosting capacity constraints and planned grid augmentation.

[9] Originally scheduled to be operational in 2025.

[10] Estimated at June 2025 in the 2022 ISP, compared to current estimates of sometime in 2027.

[11] Adapted from: htp-project-on-a-page-nov-2023.pdf (nsw.gov.au)

[12] CIS Tender 1 - NEM Generation (aemoservices.com.au)

[13] Joint media release: Big boost to reliable renewables in NSW | Ministers (dcceew.gov.au)

[14] Hosting capacity represents an indicative level of transmission capacity into/out of a REZ, usually on a “firmed” basis to account for intermittency of wind and solar

[15] FAQs - Victorian Big Battery

[16] Frequency Control Ancillary Services

Related insights

Get our thought leadership directly to your inbox

Keep up to date with the latest insights on net zero, climate resilience and clean energy transition.